Market predictions are foolish. All of us realized this a very long time in the past. However that doesn’t imply they’re fully nugatory. Though forecasts are nearly all the time fallacious, they are often entertaining and academic. That’s all I’m making an attempt to do with this publish. Entertain and educate. Evidently, however I’ve to say it anyway, nothing on this record is funding recommendation. I’m not doing something with my portfolio based mostly on these predictions, and neither must you.

Right here is my record from a 12 months in the past. I received some proper and a some fallacious. I anticipate my predictions to have a horrible monitor file, and that’s why I attempt to trip the market moderately than outsmart it. So why am I doing this? Nicely, it’s enjoyable to look again on what you thought was potential a 12 months in the past. If you see that you simply had been so off on some issues, it reminds you simply how troublesome it’s to foretell the long run. I additionally be taught so much by doing this. I uncovered some issues that I didn’t know or forgot I knew. So with that, these are my ten predictions for 2024.

- No consolidation in media/streamers.

- Apple will get dropped from the magnificent 7. Netflix Replaces it.

- Amazon features >25%/Microsoft turns into the primary $4 trillion inventory.

- Robinhood will get acquired

- Cash stays in cash market funds

- Inflation will get to the Fed’s goal. The financial system overheats. Inflation picks up.

- The vibecovery begins

- No recession. Shares achieve 20%. Giant-cap tech rolls on. The opposite 493 and small caps catch up.

- Bitcoin hits 100k

- Compulsory, one thing comes out of nowhere that makes not less than half of those predictions look very dumb.

No consolidation in media/streamers.

My first prediction is the one which may change into fallacious the quickest. Final week, a day after I informed Josh he was loopy for pondering that WBD would purchase Paramount, we received information that the 2 had been having exploratory talks to merge. I don’t purchase it, sorry, and the market doesn’t both. Since that information got here out, Paramount’s inventory has fallen 5%, and Warner Brothers Discovery is down 2%. The market is up 1% over the identical time.

These corporations are in serious trouble and the decline is structural, not cyclical. Within the first quarter of the 12 months, TV suppliers in america misplaced 2.3 million prospects, its worst displaying ever. Describing the state of the trade, SVB MOffettNathanson senior analyst Craig Moffett wrote, “We’re watching the solar starting to set.”

WBD networks (TNT, CNN, TLC et al) income fell 7% y/o/y in the newest quarter. The debt state of affairs isn’t nice both. WBD has $43 in debt and $2.4 billion in money with slightly below $3 billion maturing on common yearly over the following 5 years.

Right here is the share worth of WBD because it spun out of AT&T within the spring of 2022. Even a $1.4 billion blowout from Barbie couldn’t save this inventory.

Paramount isn’t in a significantly better state of affairs. Their inventory has additionally been greater than lower in half over the identical time because the enterprise tries to determine the place to go from right here.

Paramount+ subscription income grew 46% within the third quarter to $1.3 billion, however the firm continues to be dropping cash. Within the 9 months ended 9/30 of this 12 months, their adjusted OIBDA (???) was -$1.173 billion, barely higher than the $1.244 billion loss over the identical time in 2022. It’s not stunning that the market killed a inventory whose predominant enterprise is in secular decline, whereas its tried pivot continues to be dropping ten figures.

So why precisely would these corporations be stronger collectively?

Right here’s what Wealthy Greenfield needed to say with Matt Belloni on The City:

The factor that nobody’s speaking about is Viacom merged with CBS. That’s how we received Paramount at this time. The inventory is dramatically decrease. Warner Media, which was a part of AT&T received merged into Discovery. It’s dramatically decrease than when it merged. So 1+1 on either side has equaled .5 or much less. Now we’re speaking about placing .5 and .5 collectively and can we find yourself with .1? Everyone seems to be form of lacking that placing issues collectively just isn’t the reply right here.

What I feel is a extra probably state of affairs is that these corporations get smaller, not greater. Lucas Shaw reported that Paramount is in talks to promote BET. I’m unsure if there are non-public fairness consumers for issues like Nickelodeon, MTV, or Comedy Central, however perhaps this can be a state of affairs the place the sum of elements is larger than the entire.

Streaming is a troublesome enterprise. The losers had been late, and now the buyer is hitting a wall with what number of platforms they’ll pay for. Cancellations hit 5.7% in October, the very best on file. So yeah, linear TV is in secular decline and customers are saying no mas to extra month-to-month streaming payments.

The streaming wars are over. There’s Netflix, Amazon, YouTube, and all the pieces else. Disney/Hulu aren’t far behind, however I’ve already gone too lengthy on the primary prediction.

So no, I don’t suppose Paramount or WBD or discover a lifeline. I additionally don’t know that I’d wager in opposition to their shares. Certainly all the pieces I simply wrote is well-known by actually each market participant. I additionally don’t know that I’d purchase their shares right here, as tempting as a 50%+ drawdown is. Absent a purchaser, I simply don’t know what the catalyst can be to re-rate these shares larger, given the structural declines of the companies. I’m excited to see how this story performs out.

Apple will get dropped from the magnificent 7. Netflix Replaces it.

Apple the enterprise didn’t have a fantastic 12 months. Within the final twelve months, income is down, bills are up, and working earnings is down. Earnings per share are up a penny as a result of they’re shopping for again a lot inventory.

Whereas the enterprise has struggled to develop, the inventory delivered one other phenomenal 12 months for its shareholders. Apple goes to complete 2023 simply shy of a 50% achieve. Since 2010, it’s delivered a median annual return of 31%, 18% higher than the S&P 500. Actually certainly one of if not the very best runs any inventory has ever had.

Apple’s inventory shined even because the enterprise waned because of a number of growth. It got here into 2023 buying and selling at 21x TTM earnings and exited at 31x. Now definitely a few of that was partly attributable to the truth that companies, a really excessive margin enterprise, was 25% of gross sales in the newest quarter, up from 21% a 12 months in the past. However even nonetheless, valuations are considerably larger than they’ve been for the final decade with out the entire progress to assist it.

Apple is clearly one of many largest and finest corporations of all-time. However perhaps with a market cap of $3 trillion and progress waning, it’s time for his or her shares to take a breather.

Giant tech may have one other good 12 months, however Apple received’t. They may underperform the S&P 500 by greater than 10%, and might be faraway from the Magnificent Seven. Taking their place would be the winner from the streaming wars, Netflix (a inventory I personal).

May 2023 look any totally different from 2022 for Netflix the enterprise and the inventory? It’s wonderful that for as a lot as we speak about Netflix, we would not speak about this angle sufficient; Its rise and fall and rise once more.

This little streaming enterprise introduced Hollywood to its knees.

As Netflix garnered tons of of thousands and thousands of subscribers and added tons of of billions in market cap, the incumbents scrambled to catch up. However then one thing attention-grabbing occurred; we realized that streaming wasn’t such a fantastic enterprise for everyone however Netflix. Traders regarded previous that throughout the ZIRP/covid period, and these corporations and shares got the good thing about the doubt. Don’t fear about {dollars}, give attention to progress! And so they did.

However when Netflix reported that it misplaced subscribers final 12 months, its inventory tanked and it took the remainder of the trade down with it. The incumbents had been chasing a automotive going 100 mph proper earlier than it crashed right into a wall. Just like the scene in Go away the World Behind, all of the vehicles piled up behind them.

Netflix shed 75% peak-to-trough and ended up falling 51% in calendar 12 months 2022. In 2023, because it targeted on progress by way of an ad-supported tier and killing password sharing, its inventory sharply rebounded, gaining 64% on the 12 months.

In 2024 it would rejoin the Magnificent Seven, after being faraway from FANMAG a few years in the past.

Amazon features >25%/Microsoft turns into the primary $4 trillion inventory.

Do you know that Amazon has underperformed the S&P 500 during the last 5 years?

Amazon’s inventory hasn’t hit an all-time excessive in 624 days, by far the longest streak since 2009.

The inventory has been beneath strain for professional causes. 23% of Amazon’s income comes from abroad, which has skilled an working lack of $4.5 billion during the last twelve months.

What’s weighed on Amazon’s shares most of everywhere in the final couple of years is that Amazon Internet Companies, the section that’s been accountable for the lion’s share of the earnings, has been slowing as Microsoft and Google have been fiercely competing for the enterprise.

And regardless of its challenges, Amazon’s free money flows have had a dramatic turnaround.

And regardless of its challenges, Amazon’s free money flows have had a dramatic turnaround.

Very like Netflix, Amazon is ready to earn some huge cash by way of advertisements by means of its streaming service, which is ready to drop in January. At a $40 billion run fee, Amazon is already one of many largest promoting companies on the earth.

Amazon has been left within the mud by the remainder of the magnificent seven. In 2024, its shares will achieve 25% and hit an all-time excessive. Full disclosure, I just lately purchased the inventory.

***

Microsoft is an anomaly. Its large measurement isn’t slowing down its progress.

Simply 4 years in the past in 2019, Microsoft did $126 billion in income. Its cloud division, which makes up greater than 50% of its income, is now on a $127 billion annual run fee. And the gross margins on this enterprise are an eye-watering 72%.

The most important driver of the cloud enterprise, Azure, continues to be rising at 28% a 12 months. And we haven’t even begun to see how AI, which Microsoft is nicely positioned for, will add to its backside line.

$4 trillion admittedly seems like a stretch, however we’ll test again in twelve months.

Robinhood will get acquired

The wealth administration trade was dealing with substantial headwinds coming into 2023 for the primary time in a very long time. In a 12 months like 2017, when purchasers can earn lower than 1% on their money whereas the S&P 500 features 20%, monetary recommendation is in excessive demand. In a 12 months like 2023, when you possibly can earn 5% on money and the S&P 500 enters the 12 months in a 20% drawdown, money is stiff competitors.

That is how an organization like Morgan Stanley can see their internet new property decline by 45% year-over-year.

The secret in wealth administration is buyer acquisition. And everyone seems to be all the time trying to appeal to the following technology of purchasers, who’re set to inherit trillions of {dollars} over the approaching years. By 2045, millennials and gen X are projected to regulate 80% of all non-public wealth.

That’s why Robinhood and its 23 million accounts are such a sexy asset (10.3 million month-to-month lively customers). Certain, the typical steadiness is beneath $4,000, however that’s the chance. What number of prospects does Robinhood have who view that as their play account? What’s the typical internet value of those prospects? And what’s that going to be 5 and ten years from now?

With an enterprise worth of $6.8 billion, that represents an acquisition value of $294 per account ($658 per month-to-month person). Robinhood solely generated $77 per account ($172 per month-to-month person) during the last twelve quarters. If a purchaser thinks they’ll make these numbers converge, then an acquisition right here can be a steal.

Now, whether or not or not an organization like that or every other needs to be related to meme buying and selling and all that, nicely that may be sufficient to maintain them away.

Robinhood’s inventory has been useless cash, falling 63% from its IPO in 2021.

However one factor that Robinhood does have going for it’s that like most money-losing corporations, it has been working onerous to turn into worthwhile, and will get there subsequent 12 months.

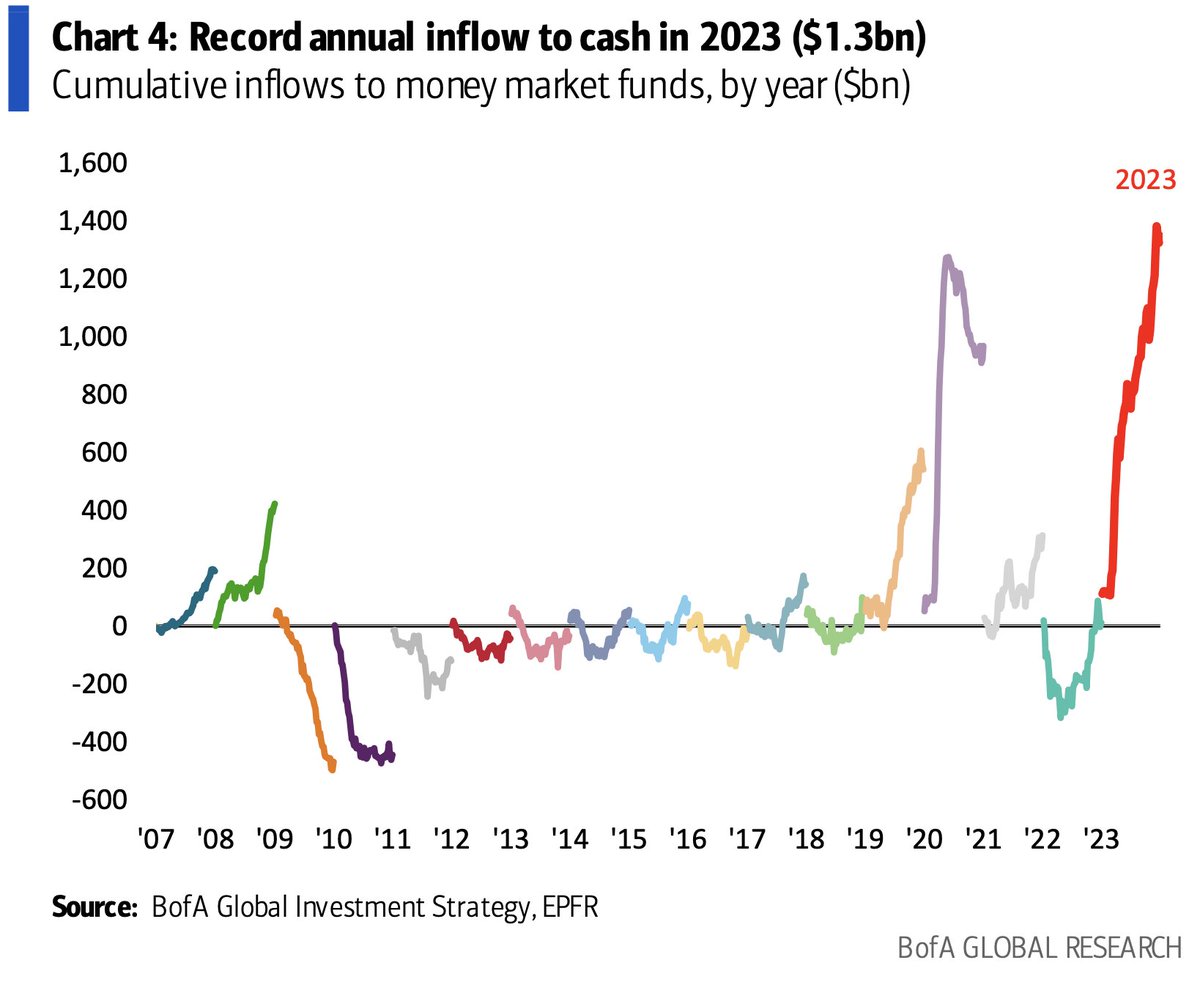

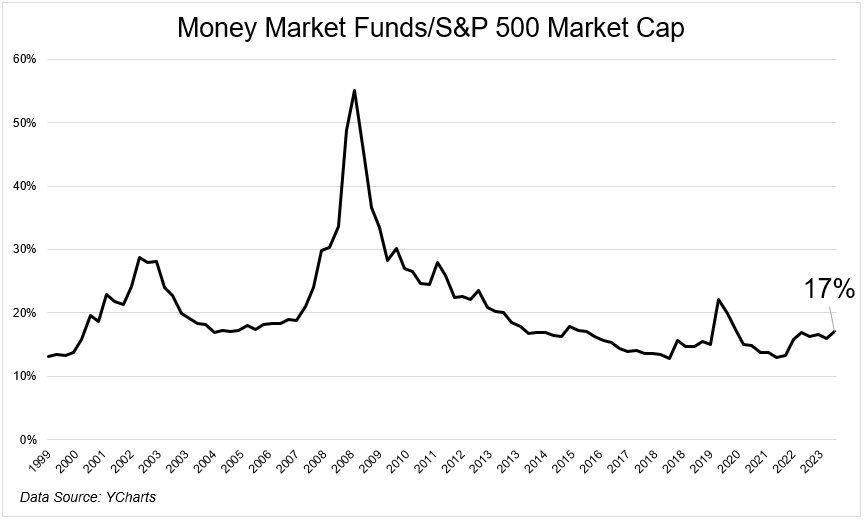

Cash stays in cash market funds

There may be some huge cash in cash market funds. Over six trillion to be exact. And one-quarter of all these property flowed there in 2023 because the risk-free fee soared to five%.

Initially of December, I requested Eric Balchunas for some information right here and he shared a mind-blowing stat; Fourteen cash market funds have taken in over $20 billion every in 2023, and the High 12 and 25 of the highest 30 flow-getting mutual funds are cash market funds. The tidal wave of cash shifting into higher-yielding devices is a fee story, not a inventory market one.

Cash rushed out of the market and into money throughout The Nice Monetary Disaster. That’s not even near what occurred in 2023.

Cash market fund flows, and I can’t show this, got here from checking and saving accounts that had been producing nearly nothing. So even when charges come down, and even when the market continues its momentum, cash market funds will retain many of the flows from 2023. Actually I anticipate leakage in some unspecified time in the future if the fed cuts, and extra if the market rips, however I’d wager that that cash is stickier than some would suppose.

Inflation will get to the fed goal. Economic system overheats. Inflation picks up.

What an unimaginable trip the financial system has been on over the previous couple of years. We received used to a world with low inflation and the low-interest charges that accompanied it. After which the pandemic occurred and shattered the financial system as we knew it. An excessive amount of stimulus led to an excessive amount of demand. Combine all that with too little provide and also you get an atomic response.

CPI isn’t removed from the Fed’s 2% goal, and it’s already there when you use a extra present measure of shelter inflation.

More often than not the Fed raises charges as a result of they need to settle down the financial system. They need to cease it from overheating as a result of there’s extra within the system. That’s probably not what occurred this time round. Certain there have been extra financial savings, however, and I’m making this up, I’d guess that greater than, and I can not stress sufficient that I’m making this quantity, 70% of the inflation we skilled was attributable to provide chain-related points. So the slowing of extra that hardly existed wasn’t a lot of a think about bringing down inflation.

All that is to say that we danger seeing an overheated financial system if the Fed begins to chop, which the market thinks it would. The overheating will come from two of the largest elements of the financial system that affect shopper spending; homes and shares.

The market is at present implying an 80% likelihood that the decrease vary of fed funds might be under 4% this time subsequent 12 months. I’ll take the beneath on that.

Sentiment/vibes enhance.

We spent a lot time questioning and debating why there was a big cap between how the financial system was doing and the way folks felt about their private monetary conditions. The disconnect isn’t as sophisticated as we would have made it out to be. It’s inflation, interval. Certain there are different issues to contemplate however they’re simply the toppings whereas costs are the complete slice. Squeezing a decade’s value of worth will increase into simply two years will destroy shopper morale. In a wholesome financial system, folks don’t change their spending habits. They only spend greater than they used to for a similar factor. And it pisses them off.

2024 will nonetheless be crammed what scary headlines. Social media will proceed to rot away on the cloth of our society. And I’m certain the election season might be as terrible as ever. However so long as costs cease going up, then the entire typical issues that factored into the vibecession will fall by the wayside.

John, our Senior Inventive Media Producer shared this on Slack the opposite day. “Vibes test. Simply received my yearly lease paperwork dropped off to my door. No lease improve, identical lease for the renewal – first time ever, I’ll take it!”

John is only one of 45 million households in america who will get to expertise this win in 2024.

Sure, rents are nonetheless up a ton, as you possibly can see under. However they’re coming down, and typically the route is extra essential than the extent.

The vibecovery begins in 2024.

No recession. Shares achieve 20%. Giant-cap tech rolls on. 493 and small caps catch up.

Giant shares beat the crap out of all the pieces else in 2023. There was a 13% unfold between the cap and equal-weighted variations of the S&P 500, ok for the second strongest calendar 12 months ever, exterior of 1998. I’d be very shocked if this continued subsequent 12 months.

The rationale for the hole was fairly easy. It was pushed by totally different exposures to sectors of the market. Having a large underweight to tech and communication companies, which gained 56% and 52% final 12 months will definitely go away a mark.

Folks spent the complete 12 months speaking about the way it was solely the magnificent 7 that had been carrying the market. And that was true for many of the 12 months! The equal-weight index was flat on the 12 months by means of November ninth. Nevertheless it ended 2023 up 14% with an incredible winter rally.

I’m not predicting massive tech to have a troublesome 12 months as I’m bullish on 2024 (I cringed writing that), however I do suppose the S&P 493 will outperform the S&P 7 as larger rates of interest are extra of a headwind for corporations with out trillion greenback market caps and tons of of billions of {dollars} in money.

Valuations are by no means a catalyst and the timing of when (if?) they matter is hardly a settled matter. Nonetheless, the unfold right here is fairly dramatic.

The market completed the 12 months with a bang. The S&P 500 was up 9 straight weeks for the primary time since 2004.

You may be questioning what historical past says in regards to the 12 months following a 20% achieve, which has occurred 19 instances since 1950. It was larger the following 12 months 15 instances, with 10 of 19 seeing a double-digit achieve. This can be a very small pattern measurement to be rendered inconclusive.

The S&P 500 will achieve 20% subsequent 12 months. The equal weight will achieve extra.

I in all probability may have stated extra on this one, however after three thousand phrases I’m working out of steam.

Bitcoin hits 100k

You may suppose that with a 150% achieve in 2023, the ETF information is priced in. You may additionally bear in mind the runup in 2017 when the CME launched its Bitcoin futures buying and selling, which marked a fairly vital prime.

I don’t anticipate the ETF to be a sell-the-news occasion as a result of there might be tens of billions of {dollars} of shopping for strain now that buyers can get entry to Bitcoin by means of their car of selection. Bitcoin is a provide and demand story, and 60% of the provision has been held by buyers for greater than 1 12 months, the very best fee ever (h/t Tom Dunleavy). These folks don’t promote.

I’m of the straightforward view that subsequent 12 months demand will vastly outpace provide, pushing the worth so much larger.

One thing comes out of nowhere that makes not less than half of those predictions look very dumb.

Ben Graham as soon as stated, “Practically everybody involved in widespread shares needs to be informed by another person what he thinks the market goes to do. The demand being there, it should be provided.”

Predictions are inconceivable. Everybody is aware of this, I hope.

If you happen to reframed the query of “What do you suppose the market will do subsequent 12 months” to “Do you suppose you possibly can predict the long run,” then perhaps it might turn into extra obvious how foolish all of that is. After all no person can predict the long run. After all no person is aware of what the market goes to do subsequent 12 months.

I encourage everybody to make a listing like this. It can function a reminder twelve months from now about how fallacious you had been about so many issues, and hopefully that can encourage you to not put money into a approach that counts on you getting the following twelve months proper.

Thanks everybody for studying. Wishing you the very best in 2024.

Nothing on this weblog constitutes funding recommendation, efficiency information or any advice that any explicit safety, portfolio of securities, transaction or funding technique is appropriate for any particular particular person. Any point out of a selected safety and associated efficiency information just isn’t a advice to purchase or promote that safety. Any opinions expressed herein don’t represent or indicate endorsement, sponsorship, or advice by Ritholtz Wealth Administration or its staff. Ritholtz Wealth Administration and its associates might put money into any firm mentioned.