The U.S. housing market has had a tumultuous few years. After falling to file lows through the pandemic, the common 30-year mortgage fee quickly elevated in 2022 and 2023 and now hovers close to a two-decade excessive of seven.2 %. For those who locked in a low mortgage fee previous to 2022, this steep enhance has considerably elevated the price of shifting, as taking out a mortgage at present charges would doubtlessly enhance their month-to-month housing cost by a whole bunch or hundreds of {dollars}, even when the quantity they borrowed remained unchanged. As proven by Ferreira et al. (2011), this lock-in impact has the potential to scale back geographic mobility and turnover within the housing market and has gained the eye of Federal Reserve leaders. On this put up, we make the most of particular questions from the Federal Reserve Financial institution of New York’s 2023 and 2024 SCE Housing Surveys to estimate the extent to which mortgage fee lock-in is suppressing U.S. family’s shifting plans.

U.S. Householders Plan to Keep Put

In contemplating how mortgage fee lock-in is affecting mobility, it is usually price noting that shifting charges are at the moment fairly low in the US. Whereas declining mobility intensified barely in recent times, Koşar et al. (2022) present that it isn’t only a pandemic-era phenomenon. For instance, shifting charges have been steadily declining for many years and had been already beneath 10 % in 2019, whereas they had been shut to twenty % within the mid-Eighties. Frost (2023) reveals that switching residences is even rarer for owners, whose shifting charges have been certain between 5 % and 10 % annually since 2006. With such low shifting base charges, it’s unclear if we must always count on mortgage fee lock-in to considerably cut back geographic mobility.

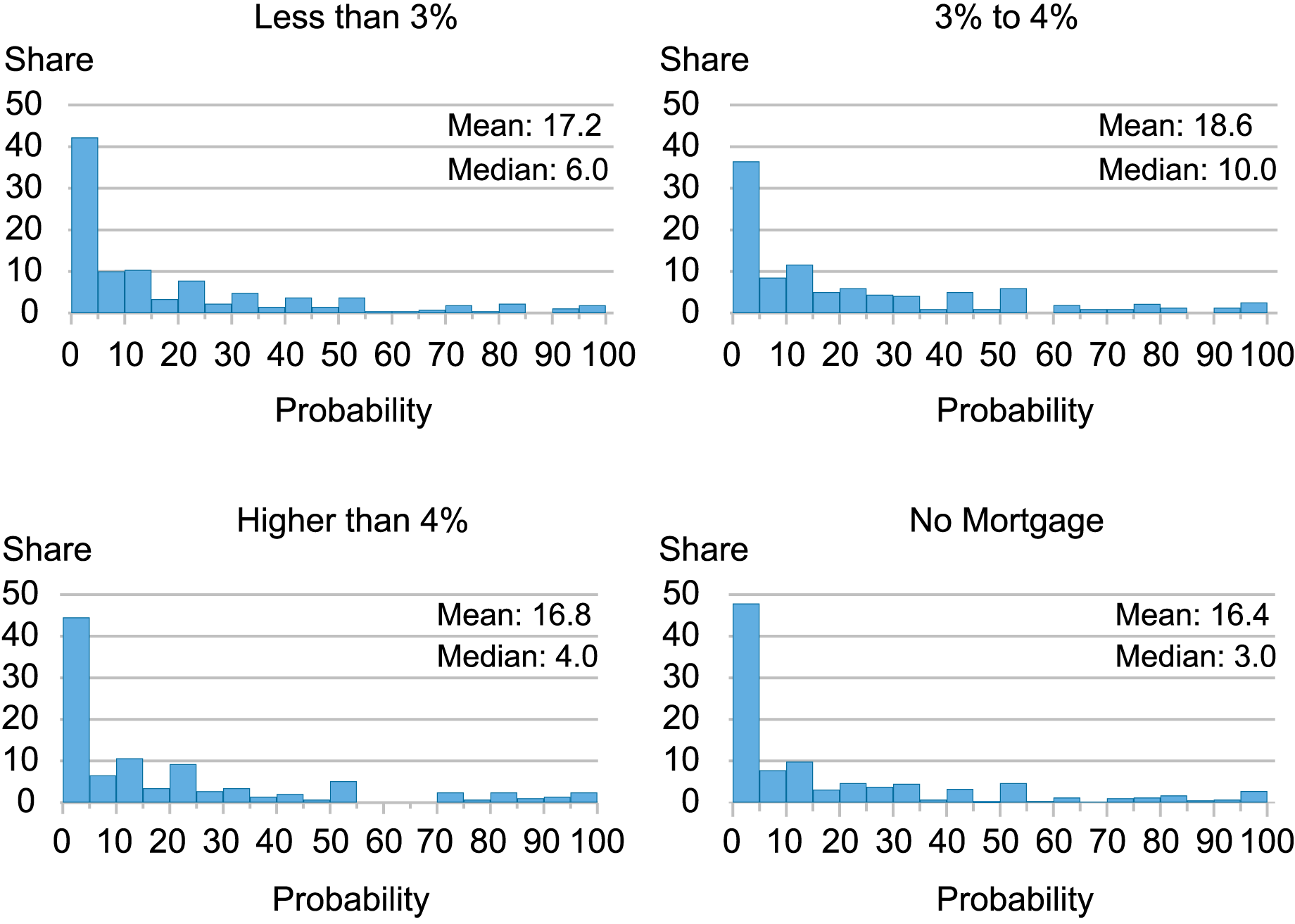

To evaluate the affect of mortgage fee lock-in on home-owner’s shifting plans, we first requested respondents who at the moment personal a house for the % likelihood that they’ll transfer within the subsequent three years. As proven within the histograms beneath, U.S. households’ shifting plans usually mirror the decline in mobility that we’ve seen in latest many years. Throughout the distribution of householders’ present self-reported mortgage charges, near half of respondents assess their chance of shifting within the subsequent three years to be lower than 10 %, with nearly three-quarters of respondents inserting their possibilities at lower than 25 %.

These patterns are broadly constant throughout owners with and with no mortgage, as all teams report a imply chance of shifting within the subsequent three years between 16 % and 19 %. Though these comparisons don’t take variations of different traits between the teams under consideration, they’re suggestive that few U.S. owners are planning to maneuver within the subsequent three years and are akin to the precise charges of annual mobility we reported above.

Distribution of Self-Assessed Chance of Transferring in Subsequent Three Years by Present Mortgage Fee

Be aware: Figures don’t embrace renters.

Estimating the Lock-In Impact

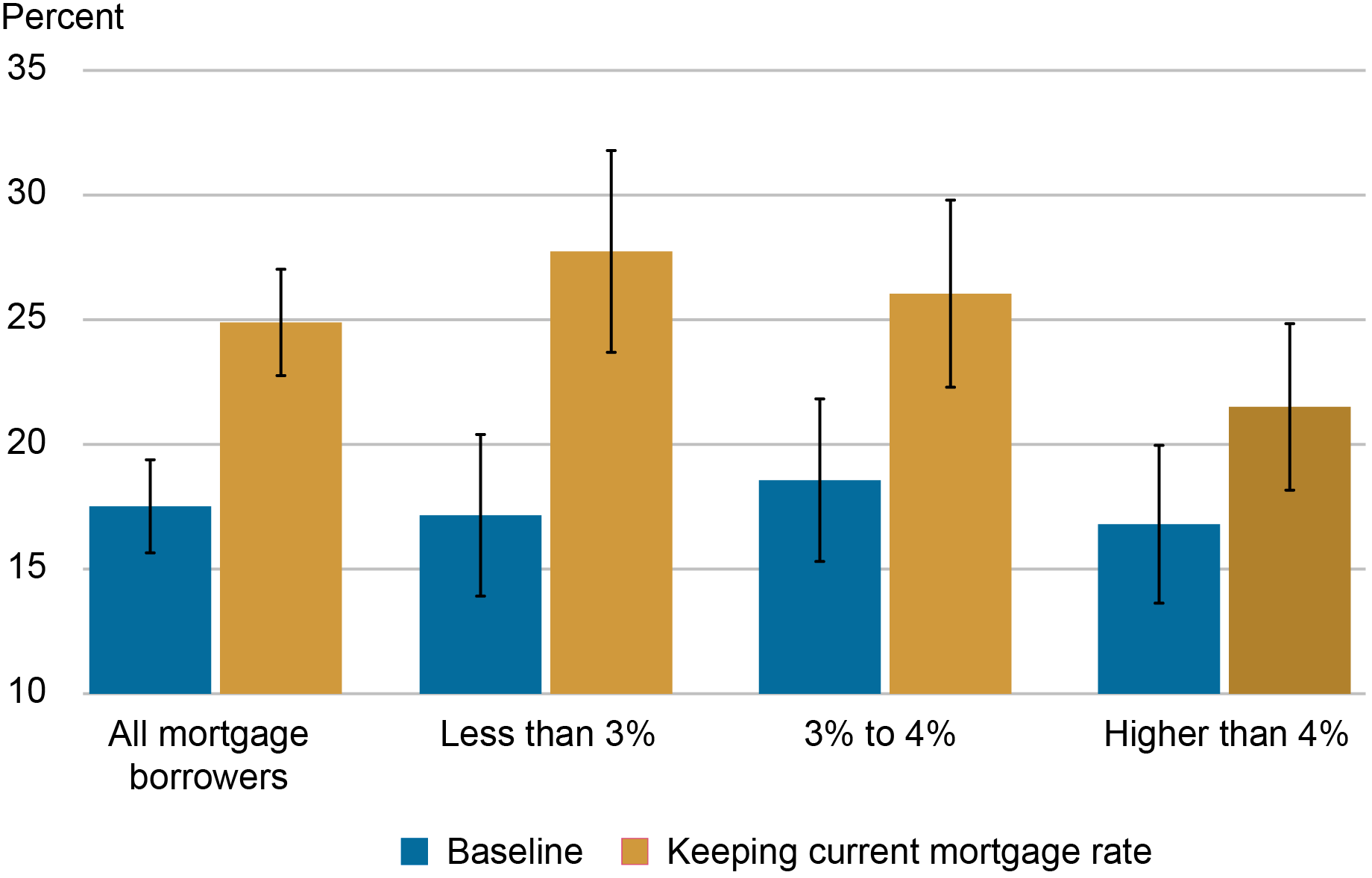

To know the extent to which the lock-in impact is suppressing family’s shifting plans, we offered owners with a mortgage with a hypothetical situation through which they’re provided the choice to maintain their present mortgage fee in the event that they had been to maneuver and purchase one other dwelling. We then requested them for the prospect that they might transfer within the subsequent three years beneath this situation.

As proven within the chart beneath, the flexibility to maintain one’s present rate of interest has a major impact on respondents’ shifting plans, as mortgage holders revise their chance of shifting upward by 7.4 share factors on common. This impact is especially massive for these with comparatively low mortgage charges, as people with charges beneath 3 % revise their common chance of shifting up from 17.2 % to 27.7 %, and people with charges between 3 % and 4 % report a rise from 18.6 % to 26 %. These variations are each statistically important and signify 61 % and 39.8 % will increase respectively.

As one may count on, these revisions lower monotonically with a respondent’s present mortgage fee, and people with mortgage charges already above 4 % don’t see a statistically important enhance. That mentioned, you will need to word that this result’s largely pushed by a couple of quarter of householders. Actually, near half of respondents don’t revise their shifting chance in any respect, and about 73.4 % revise their chance by 10 share factors or much less. We interpret this to imply that mortgage charges will not be a main consider most respondents’ relocation plans for the subsequent three years however are a big constraint for a comparatively small however important share of householders.

Common Chance of Transferring in Subsequent Three Years by Present Mortgage Fee

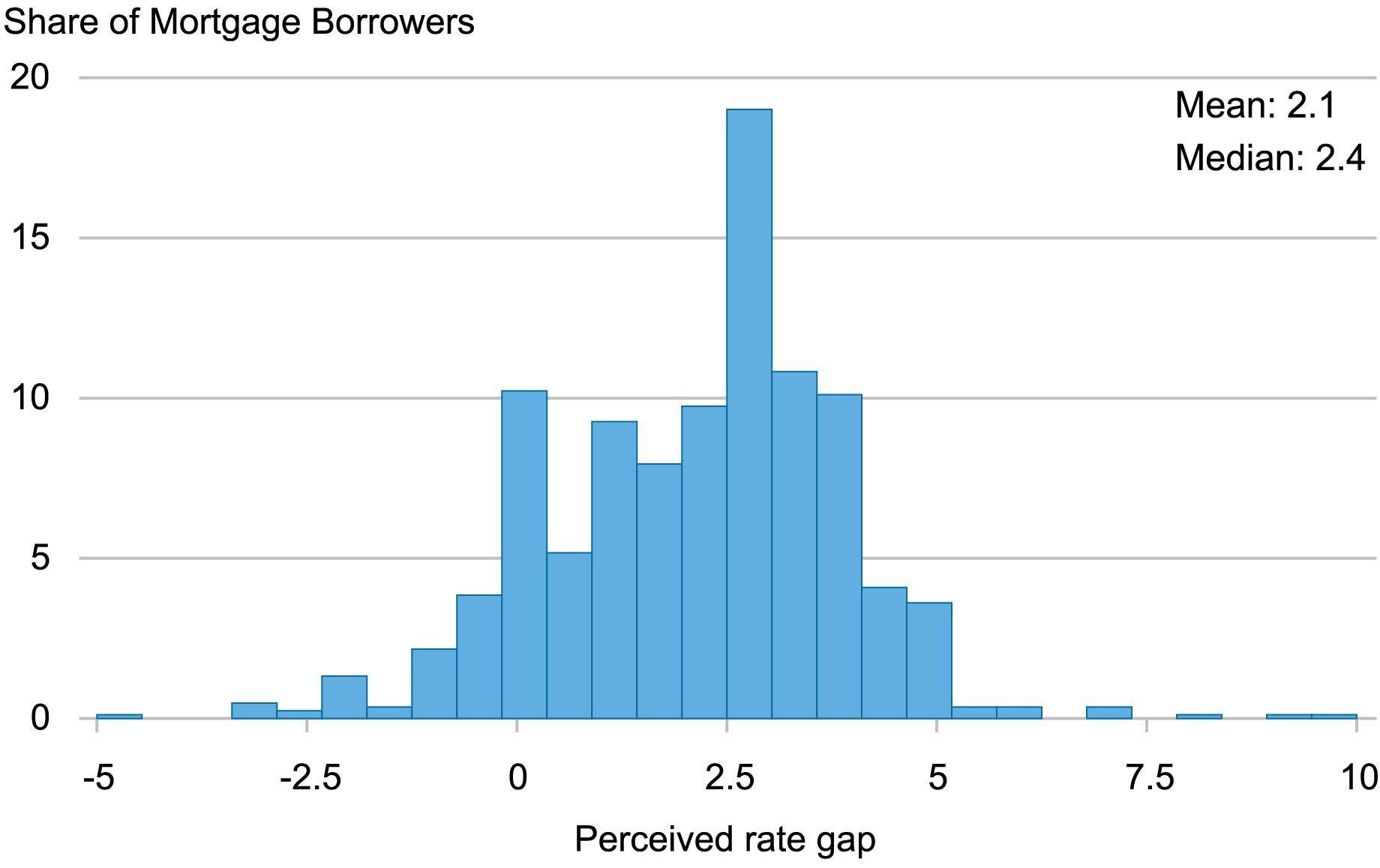

Maybe a extra intuitive approach to interpret our outcomes is thru the lens of a respondent’s perceived mortgage fee hole, which we outline because the distinction between their notion of the speed they might obtain on a brand new mortgage at the moment, and their present mortgage fee. The chart beneath reveals that the distribution of perceived fee gaps is essentially optimistic, as respondents usually count on that they would want to take out the next mortgage than they at the moment have in the event that they had been to maneuver. About 9 % report destructive perceived fee gaps, indicating that they consider they may get hold of a greater fee than they’ve now. This might point out that their private circumstances have modified since they obtained their mortgage. For instance, a few of these people could have lately seen will increase of their credit score scores.

Distribution of Mortgage Debtors’ Perceived Mortgage Fee Gaps

Be aware: A respondent’s perceived mortgage fee hole is outlined because the distinction between their notion of the speed they might obtain on a brand new mortgage at the moment and their present mortgage fee.

To place our outcomes by way of respondents’ perceived fee gaps, contemplate that at baseline, they report a mean chance of shifting within the subsequent three years of 17.5 %, and a mean perceived mortgage fee hole of two.1 share factors. In our hypothetical situation, we set their perceived hole to zero share factors and see their common chance of shifting rise to 24.9 %. If we contemplate these results linearly, this means {that a} one share level lower in a person’s perceived mortgage fee hole is on common related to a couple of 3.5 share level enhance of their self-assessed chance of shifting within the subsequent three years.

Will Lowering Mortgage Charges Improve Mobility?

Non-public forecasters anticipate that the federal funds fee will decline in some unspecified time in the future sooner or later, with mortgage charges usually anticipated to comply with go well with. Our outcomes counsel that these reductions would spur some enhance in relocations. That mentioned, most householders in our survey don’t appear to be making their shifting plans primarily based on mortgage charges. For many who are, the impact of fee cuts on their mobility will in the end rely upon their beliefs concerning the fee they might qualify for on a brand new dwelling. Certainly, understanding how households type perceptions of the housing market can be an thrilling space of analysis going ahead, and vital to understanding the extent to which the lock-in impact reduces mobility.

Felix Aidala is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Andrew F. Haughwout is the director of Family and Public Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ben Hyman is a analysis economist in City and Regional Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jason Somerville is a analysis economist in Client Conduct Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is the financial analysis advisor for Family and Public Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How one can cite this put up:

Felix Aidala, Andrew Haughwout, Ben Hyman, Jason Somerville, and Wilbert van der Klaauw, “Mortgage Fee Lock‑In and Householders’ Transferring Plans,” Federal Reserve Financial institution of New York Liberty Avenue Economics, Could 6, 2024, https://libertystreeteconomics.newyorkfed.org/2024/05/mortgage-rate-lock-in-and-homeowners-moving-plans/.

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).