There’s a lot we are able to’t clarify:

What’s the universe product of? (Trace: it doesn’t really appear to be “matter and vitality”)

What lives within the ocean’s “twilight zone”? (“It’s distant. It’s deep. It’s darkish. It’s elusive. It’s temperamental,” in response to Woods Gap … maybe probably the most mysterious and very important area on the planet)

What killed Venus? (The planet, not the goddess. Greatest guess is that it as soon as had a water ocean and now has a 900-degree floor temp … virtually scorching sufficient for Florida to grant warmth breaks to staff!)

Who thought it was a good suggestion to solid John Wayne as … Genghis Khan? (The Conqueror, 1956, was filmed on a fallout-contaminated set close to a nuclear bomb testing vary and featured traces like “I really feel this Tartar lady is for me, and my blood says, take her. There are moments for knowledge and moments once I take heed to my blood; my blood says, take this Tartar lady.”)

Who thought it was a good suggestion to solid John Wayne as … Genghis Khan? (The Conqueror, 1956, was filmed on a fallout-contaminated set close to a nuclear bomb testing vary and featured traces like “I really feel this Tartar lady is for me, and my blood says, take her. There are moments for knowledge and moments once I take heed to my blood; my blood says, take this Tartar lady.”)

Why do people have such massive butts? (No different mammal managed the feat.)

How does Tylenol kill ache? (And why does it induce loopy risk-taking conduct?)

Why do buyers favor low-return / high-volatility shares to their opposites?

The High quality Anomaly

In dissecting the drivers of funding efficiency, researchers level to a set of six or seven components that designate what’s occurring. Momentum. Worth/development. Excessive/low volatility. Small cap/massive cap.

By far probably the most highly effective and puzzling of the components is High quality. Morningstar’s Ben Johnson (2019) described it as “the fuzziest issue you can see within the investing world.” Ben Inker, head of asset allocation at GMO (2023) referred to as it “the weirdest market inefficiency on the earth.”

The broadest sense of a high quality firm is one which makes use of its assets prudently: high quality firms are inclined to have little or no debt, substantial free money flows, regular and predictable earnings, and maybe excessive returns on fairness. Passive methods and plenty of lively ones have a powerful backward focus: they restrict themselves to corporations which have shiny pasts, with out actively inquiring about their future prospects.

Nonetheless, the proof is compelling that high-quality shares bought at affordable costs (Mr. Buffett’s “great firms at truthful costs” best) are concerning the closest factor to a free lunch within the investing world. Normally, it’s a must to pay in your lunch a method or one other. The one rationale for getting crazy-volatile investments (IPOs, as an illustration) is the prospect of crazy-high returns. The one rationale for getting modest returns (three-month T-bills) is the promise of low volatility.

With high quality shares bought at an inexpensive value (name it QARP), that tradeoff doesn’t happen. QARP shares provide each increased long-term returns and decrease volatility than run-of-the-mill equities. GMO’s analysis bears this out throughout a span of three many years:

- Excessive-quality shares provide 60% increased returns and 30% decrease volatility than low-quality shares.

- Excessive-quality cyclical shares provide 200% of the returns with 30% decrease volatility than low-quality cyclicals.

- Excessive-quality small-cap shares provide 150% of the return of low-quality ones with 30% much less volatility.

- Excessive-quality worth shares provide 150% of the returns of low-quality ones with 30% much less volatility.

- Excessive-quality (BB) junk bonds provide 300% of the returns and 50% decrease volatility than low-quality (CCC) junk bonds.

(Supply: GMO, “The High quality Anomaly,”2023, displays 1-3, 5 and 6. In every case we approximated share values from their graphs)

Different researchers discover an similar sample in rising Europe and in rising markets typically: “The standard basket generated a compounded annual return of 15.0% as in comparison with 8.4% for MSCI EFM Normal index. What’s extra, annualized commonplace deviations of month-to-month returns had been decrease for the standard basket at 14.2% as in comparison with 23.4% for the benchmark index” (Ramraika and Trivedi, “Excessive High quality Shares in Rising Markets,” 2015). In “most [world] areas and dimensions … our high quality issue delivers a statistically important alpha that can not be defined by loadings on typical fairness components akin to market, worth, measurement, and momentum (Amundi Institute analysis group, “Revisiting High quality Investing,” 2024).

There isn’t a clear clarification for why high quality is so extensively, badly, and persistently mispriced. Some individuals declare that “high quality” wins simply because it’s a attribute of the tech sector (not true: because it additionally holds in the old fashioned cyclical firms, too) or that it wins due to the ability of mega-cap monopolies (not true: because it additionally holds in small caps) or that it wins as a result of development firms are all shiny (likewise, not true: the connection holds amongst worth firms, too). Briefly, just about all over the place we glance high quality wins however sketchy shares draw consideration. One of the best that GMO’s Tom Hancock and Lucas White may provide you with is, “buyers routinely overpay for the thrilling lottery ticket prospects of speculative, junky enterprise fashions whereas neglecting the tangible however boring attributes of High quality” (“The High quality Spectrum,” 2023). Mr. Inker laments, “I’ve bother developing with something in any respect believable that doesn’t come to down ‘buyers are weirdly silly.’”

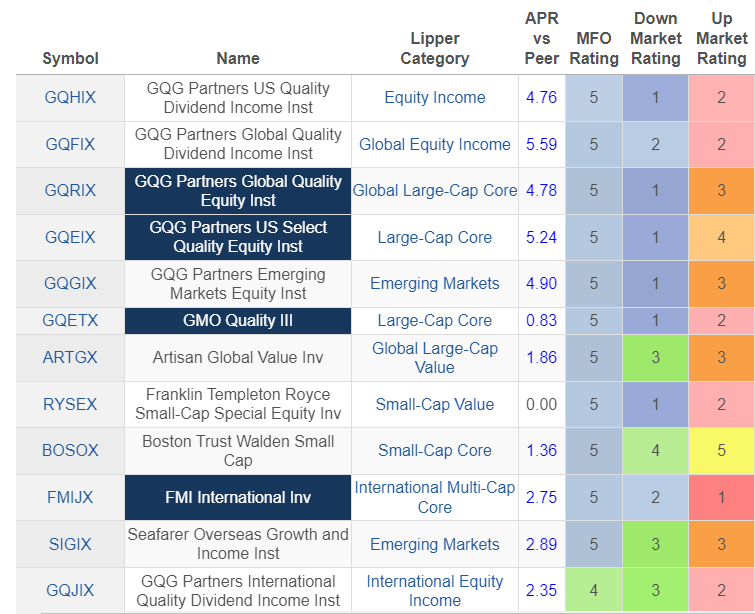

However not all the time. High quality tends to lag, nevertheless, in the course of the mid-to-late phases of a bull market as buyers (bless their hearts) begin treating low-quality / high-beta shares as lottery tickets. For visible learners, right here’s the efficiency of a wide range of funds that maintain high-quality shares. We’re charting efficiency since inception. The primary knowledge column reveals how they’ve carried out towards their friends (+2% means, as an illustration, that the fund has outperformed its friends by 200 bps/yr). The subsequent three columns illustrate how the fund carried out within the long-term (MFO ranking), throughout months when the market was falling (down seize ranking), and through months when the market was rising (up seize ranking). Right here’s the important thing: blue/inexperienced = good, crimson/pink/orange = dangerous.

Lifetime efficiency for choose high quality funds, by March 2024

With out exception, these high-quality portfolios crushed their friends in the long run and crushed their friends when markets had been at their worst. In rising markets, they made robust absolute good points whereas nonetheless trailing the overwhelming majority of their quality-agnostic friends.

High quality wins over full market cycles, partially by crushing the efficiency of low-quality shares when the dangerous occasions hit. GMO’s Ben Inker notes “high-quality shares outperform low-quality shares in down months by over thrice the quantity they underperform in up months!” Certainly, high-quality firms use crises to their benefit: they are typically debt-free and cash-rich, in order that they’ll transfer opportunistically in crises when lesser firms are folding.

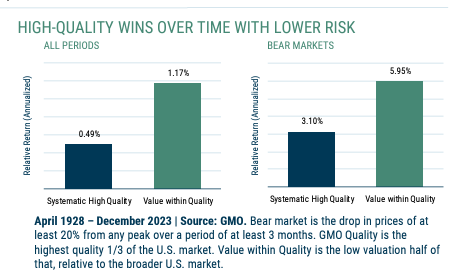

Lastly, value issues. Overpaying for a high quality firm cuts your returns and reduces your margin of security. GMO has tracked the relative outperformance of high quality shares towards the broader market again to 1928, then pulled out the efficiency of the most affordable half of the standard universe for a similar interval. The distinction is dramatic.

The quick model: high quality wins. High quality at an inexpensive value wins by rather a lot.

Choices for Including High quality to your portfolio

MFO recognized a number of distinctive high-quality funds which may help you reap the benefits of this investing anomaly. We targeted on two of probably the most distinguished households whose work mixed commitments to each high quality and worth. (We additionally partnered with the parents at Morningstar to hunt their assist in figuring out funds in a wide range of niches which may assist diversify your portfolio.)

MFO commends:

GMO US High quality Fairness ETF (QLTY), a newly launched, actively managed ETF, that operates with the identical self-discipline and identical administration group because the $10 billion, five-star Nice Owl GMO High quality (QGETX) fund. GMO grounds its High quality Technique within the work accomplished by its founders within the Nineteen Seventies and formalized in 2004.

In 2004, GMO launched the High quality Technique with the mandate to personal attractively valued shares inside the high quality universe. The creation of the technique was the end result of many years of GMO analysis on high quality enterprise fashions. Whereas the technique’s origins date again to GMO’s earliest days, our course of continues to evolve to make sure sustained relevance in addition to our funding edge.

Since its launch in November 2023, the ETF has really outperformed its elder sibling, returning 17.0% to QGETX’s 15.3%. The ETF, which prices 0.50% for its companies, has shortly gathered $600 million in property, a win that portends further GMO ETF launches. (Full disclosure: Chip, MFO’s cofounder, added QLTY to her private portfolio shortly after its launch.)

GQG Companions US Choose High quality Fairness (GQEPX), which launched in 2018, is managed by the GQG group headed by Rajiv Jain. Mr. Jain is among the many world’s most profitable fairness buyers, having constructed an enormous following at Vontobel earlier than transferring to discovered GQG: World High quality Development. The core self-discipline is identical throughout all of their methods:

GQG’s funding philosophy is rooted within the perception that earnings drive inventory costs.

The pursuit of sturdy earnings ignores the thought of conventional development and worth investing and as a substitute focuses on discovering firms we imagine have the best likelihood of compounding capital over the subsequent 5 years. This funding fashion targeted on high-quality, sturdy companies, is taken into account by GQG to be extra suitably named as “Ahead-Wanting High quality”.

The agency launched its now-$20 billion Rising Markets Fairness fund initially then added US Choose High quality Fairness and World Choose High quality Fairness about 5 years in the past. All have persistently earned five-star scores from Morningstar, all have completed within the high 1-2% for whole returns of their Morningstar peer teams over the previous 5 years, and all outperformed their Lipper peer teams by a mean of 500 bps per yr. Each US Choose and World Choose earned MFO’s Nice Owl designation for persistently top-tier risk-adjusted efficiency. These have been complemented by three high quality + dividend funds launched just below three years in the past, every of which has additionally simply outpaced their friends. Briefly, GQG will get it proper persistently, over time and throughout world markets.

GMO and GQG would possibly signify a rock-solid core for an investor’s portfolio. We reached out to Morningstar, asking for his or her tackle the best high quality fairness funds {that a} quality-sensitive investor would possibly add to such a portfolio. Robby Greengold, a Morningstar strategist, provided a dozen prospects. He defined his technique this manner:

I chosen these funds for the comparatively high-quality metrics of their portfolios (e.g., high-profit margins, low debt) and Morningstar Medalist Scores (one of many fund’s share courses should obtain both a Bronze, Silver, or Gold Morningstar Medalist Ranking, which specific our conviction within the fund’s skill to outperform on a risk-adjusted foundation over a full market cycle). The funds wanted to be lined by one among Morningstar’s analysts, and the analysts wanted to explicitly level out that the fund intentionally targets high-quality shares.

Herewith are a dozen high quality funds with Morningstar’s tackle them and our occasional asides.

|

|

Morningstar’s take |

MFO’s gloss |

|

Boston Belief Walden Small Cap Fund (BOSOX), small cap mix |

This group focuses on figuring out well-managed small-cap corporations with sustainable and predictable earnings profiles that even have affordable valuations. This technique additionally has a sustainability mandate, screening out corporations deriving important income from alcohol, coal mining, gaming, manufacturing facility farming, weapons, tobacco, and jail operations (although not fossil fuels). 70-100 names within the portfolio. The place the strategy actually shines is in danger administration. The group has a high quality focus and is valuation-conscious … to a portfolio that persistently ranks among the many least-volatile choices within the small-blend class, a powerful feat contemplating its minimal money stakes. |

It’s a terrific small-cap core fund with a ticker celebrated by readers in New England. It additionally closed to new buyers in March 2023. |

|

Royce Small-Cap Particular Fairness Fund (RYSEX), small cap worth |

This technique has a conservative, risk-aware strategy. Managers Charlie Dreifus and Steven McBoyle depend on analysis and a wholesome dose of accounting cynicism to seek out small caps whose monetary stories are free from earnings manipulation. Dreifus and McBoyle hunt for clear stability sheets, low debt, excessive returns on invested capital, and rising free money stream that exceeds earnings. The managers will sit on money, which regularly reaches double digits, making a buffer in downturns however a drag when shares rise. 35-55 names, low turnover. the fund typically has rather a lot in micro-caps. |

The lead supervisor, Mr. Dreifus, has been investing for 55 years, is 80 years outdated, and has no plans for retiring. Mr. McBoyle is about 20 years his junior and has an extended tenure with Royce. Nonetheless … |

|

MFS Worldwide Fairness Fund (MIEIX), massive mix. |

The managers depend on broad and thorough bottom-up analysis and a disciplined give attention to reasonably rising, established firms with shares buying and selling at respectable costs. The managers depend on their very own analysis and that of MFS’ massive and skilled elementary analysis group to seek out rising firms with aggressive benefits and administration groups that encourage predictable earnings and money flows, wholesome stability sheets, and powerful returns on capital. The managers focus additional up the market-cap ladder than most overseas large-blend and large-growth friends, so the portfolio’s common market cap is usually increased than the class norm. |

$20 billion in AUM with main inflows in 2023-24. Steady two-person administration group. About 75 massive cap shares with actually low turnover. |

|

John Hancock Funds Worldwide Development Fund (GOIOX), massive development |

Lead supervisor John Boselli and his group give attention to firms with excessive natural development charges, low share costs relative to free money stream, and most significantly, high quality enterprise fashions. Additionally they like firms that return capital to shareholders by way of share repurchases and dividends and shun these with the worst earnings revisions. They emphasize business fundamentals, development and stability, free money stream technology, capital allocation, incentive compensation, and valuation surprises. |

The fund continues to be managed by Wellington Administration, however long-time lead supervisor John Boselli retired on the finish of 2023. He was, by all accounts, a celebrity and recipient of a number of “Supervisor of the 12 months” awards. His two co-managers, who had been added in August 2021, now have sole duty. |

|

Artisan World Worth Fund (ARTGX), massive worth |

This group consists of worth buyers who emphasize high quality corporations with monetary power and shareholder-oriented administration. They leverage qualitative and quantitative screens to slender the funding universe to a manageable degree [and] shun corporations with poor accounting and company governance requirements, in addition to these working in markets with insufficient legal guidelines and laws. It invests in corporations of all sizes that commerce at reductions to their intrinsic worth estimates, though the main focus is overwhelmingly on large-cap shares. 40–60 shares, with place sizes weighted by conviction. Commensurate with administration’s long-term mindset, portfolio turnover is usually under 30%. When the managers can’t discover alternatives that meet their strict requirements, money can construct as much as 15% of property. |

Our final profile replace was a decade in the past, reflecting a draw back of our give attention to newer, smaller distinctive funds. We reviewed the fund repeatedly when it fell inside our ambit and concluded, in our final assessment, “We reiterate our conclusion from 2008, 2011 and 2012: ‘there are few higher choices within the world fund realm.’” This fund and its sibling Worldwide Worth had been initially managed by David Samra and Daniel O’Keefe. In 2018, they determined to divide their prices with Mr. Samra main Worldwide Worth and Mr. O’Keefe main this fund. Over the previous six years, Worldwide Worth has handily outperformed its friends whereas World Worth has barely saved tempo with them.

|

|

FMI Worldwide Fund (FMIJX), massive mix |

FMI Worldwide isn’t your typical overseas large-blend Morningstar Class providing, however it’s top-notch. It seems to be for firms with sturdy enterprise fashions and powerful administration that generate superior profitability by a full financial cycle. The fund’s coverage of hedging non-U.S. forex publicity highlights administration’s give attention to underlying enterprise fundamentals. They sometimes shrink back from corporations with excessive debt ranges however will purchase these whose regular money flows can help their leverage. Annual portfolio turnover has been under most overseas large-blend Morningstar Class friends. The group’s pickiness and valuation sensitivity present within the technique’s high-conviction portfolio, which additionally stands out. It presently holds solely 40 shares, which is lower than half the roughly 100-stock peer median. |

We profiled this fund shortly after launch, predicting “All of the proof obtainable means that FMI Worldwide is a star within the making. It’s headed by a cautious and constant group that’s been collectively for an extended whereas. Bills are low, the minimal is low, and FMI’s portfolio of high-quality multinational shares is more likely to produce a smoother, extra worthwhile journey than the overwhelming majority of its rivals.” Ten years later the one factor so as to add is “Yep, nailed it.” |

|

JPMorgan Rising Markets Fairness Fund (JMIEX), rising markets |

The strategy favors high quality development firms. The group seeks corporations that boast high quality franchises, constant earnings streams, and stable returns on fairness. They conduct in-depth elementary analysis on potential concepts and assign five-year anticipated return targets. Analysts additionally classify shares on their protection lists as premium, high quality, or commonplace, in response to the agency’s strategic classification framework, which relies on a 98-point questionnaire. Premium and high quality names function in engaging industries with restricted exterior dangers and possess robust stability sheets, good administration groups, and stable cash-flow-generation prospects whereas buying and selling names lack sustainable aggressive benefits. The overwhelming majority of property are allotted to premium and high quality names, with buying and selling names making up solely a small portion. The group’s valuation framework helps to make sure managers pay the appropriate value for the chance, though they’re ready to pay up for high quality and development. |

The fund’s efficiency has been no higher than “okay” for an extended whereas, maybe reflecting a willingness to pay extra for shares and to emphasize valuations much less. Relative to its friends and benchmark, the portfolio has stronger development but in addition – by just about each measure – increased valuations. One-, three- and five-year returns are comparatively weak, and it is advisable to exit to the 10- and 15-year home windows to see robust efficiency. |

|

GQG Companions Rising Markets Fairness Fund (GQGRX), rising markets |

Lead supervisor Rajiv Jain continues to depend on the identical inventive and profitable “high quality development” strategy right here that he has used for the reason that late Nineties. He needs reliably rising firms, however provided that they’re on stable monetary footing and have demonstrated the power to climate gradual economies. Sectors or international locations may be closely obese or underweight. Although Jain sometimes has held shares for a few years, he’ll change course shortly and decisively if he considers it acceptable. A number of years in the past he sharply diminished his stake within the client staples sector when he noticed situations turning into tougher, after which elevated it once more previously couple of years because the metrics modified. And from early 2021 to late 2022, the fund’s vitality stake soared, whereas the expertise stake plummeted. Jain and his group give attention to massive firms and search for excessive returns on fairness and property and low to reasonable leverage. Then they use elementary evaluation to analysis future development alternatives, estimate dangers, analyze the accounting to make sure its accuracy and transparency, after which estimate an inexpensive value. 4 former journalists use their investigative expertise to hunt info or traits which may not be obvious within the numbers. The technique is reasonably concentrated, with 50-70 holdings and substantial (4% to eight%) weightings within the high shares. |

Within the seven years since its launch, GQGRX has been one of many high ten EM funds or ETFs in existence. It has the fourth-highest returns of any diversified EM fund (5.4% APR) however, extra importantly, one of the best Sharpe ratio (a measure of risk-adjusted returns). Throughout a wide range of danger measures, together with draw back deviation and bear market deviation, It’s clearly a high 10 performer. This displays Mr. Jain’s self-discipline: forward-looking high quality is the primary display, valuation is the second, and every part else trails. |

|

T. Rowe Worth Worldwide Discovery Fund (PRIDX), small/mid development |

The managers give attention to firms with market caps between $500 million and $5 billion with compelling enterprise fashions and the power to generate returns above the price of capital. They search shareholder-oriented administration groups with good capital allocation expertise. They favor corporations in industries which might be rising quicker than the general economic system, which might be addressing unmet wants and including worth for patrons, and which have rational aggressive buildings. The managers make use of this self-discipline with an interesting mixture of bolder and tamer traits. On the bolder facet, they readily spend money on shares within the creating world that meet their standards and frequently construct reasonable nation and sector overweightings. On the reserved facet, they pay loads of consideration to valuations, unfold the portfolio throughout 200-250 names, and transfer at a measured tempo. This strategy gives ample upside potential with out assuming extreme danger, and it has earned good long-term outcomes at a European smaller-cap providing for non-U.S. buyers in addition to this technique. |

Snowball holds about 2% of his retirement portfolio in PRIDX, a place constructed many years in the past underneath supervisor Justin Thomson who guided the fund for 22 years. T Rowe Worth does an distinctive job in managing supervisor turnover, partially as a result of they’ve a powerful, team-oriented tradition. New supervisor Ben Griffiths has been with the agency since 2006 and has managed a small cap fund for European buyers since 2016. The fund has not been a disappointment underneath his watch, however neither has it been compelling. Over the previous 4 years, the fund has outperformed its Lipper peer group by 0.1% per yr with exactly the identical Sharpe ratio (0.46). |

|

Constancy Worldwide Discovery (FDKFX), massive development |

Supervisor Invoice Kennedy needs to personal rising firms, however he isn’t going to pay any value for them. He seems to be for firms with robust three- to five-year earnings prospects, accountable administration groups, stable stability sheets, and huge potential markets. However he needs to personal corporations which might be buying and selling at engaging valuations. Whereas loads of class rivals obtained swept up out there euphoria of 2020 and 2021, shopping for up high-multiple, low-quality names, Kennedy stayed true to his strategy. In actual fact, throughout these two years, his portfolio seemed cheaper versus friends than ever earlier than, as he didn’t comply with the gang into the more-speculative waters. |

Mr. Kennedy has managed the fund since its inception (2006) and has invested greater than 1,000,000 of his personal cash in it. |

|

Constancy Diversified Worldwide (FKIDX) |

Supervisor Invoice Bower’s funding course of has a number of strengths. He seems to be for shares with long-term earnings development potential, sturdy enterprise fashions, and deep aggressive benefits. Bower is keen to pay a modest premium for these desired traits, however not as a lot as many overseas large-growth class friends, highlighting his valuation sensitivity. He can even allocate a small portion of property to shorter-term, opportunistic concepts that will not have sturdy development prospects however are nonetheless compelling. |

Mr. Bower has been managing the fund since 2001 and has invested greater than 1,000,000 of his personal cash in it. The portfolio holds about 140 names with modest turnover. The fund tends to have returns within the high third of its friends |

|

Constancy Abroad Fund (FOSFX), massive development |

Supervisor Vince Montemaggiore employs a smart strategy with a twin give attention to high quality and valuation, although high quality comes first. With out it, he gained’t personal an organization, regardless of how low cost it might appear. To him, high quality means having a novel edge, like, amongst others, excessive limitations to entry, a low-cost benefit, or excessive switching prices. Ideally, the corporate has excessive recurring revenues and low debt ranges. He needs to personal these shares which might be buying and selling at 15% or extra reductions to his estimated intrinsic worth. |

|

|

Seafarer Abroad Development and Revenue Fund (SIGIX), rising markets |

The group has all the time targeted on corporations with sturdy development prospects and dependable earnings streams whereas contemplating money flows, stability sheets, working histories, liquidity, and valuations. The method is risk-conscious, distinctive, and engaging. The group nonetheless pursues firms with sturdy development prospects and dependable earnings streams, invests broadly throughout the market-cap spectrum, and readily permits its safety choice to lead to atypical nation and sector weightings. |

One of many core holdings in Snowball’s portfolio, with FPA Crescent. Supervisor Andrew Foster’s hope is to outperform his benchmark (the MSCI EM index) “slowly however steadily over time.” His technique is grounded within the structural realities of the rising markets. A defining attribute of rising markets is that their capital markets (together with banks, brokerages, and bond and inventory exchanges) can’t be counted on to function. In consequence, you’re finest off with corporations who gained’t want to show to these markets for capital wants. Seafarer targets (1) corporations that may develop their high line steadily within the 7-15% each year vary and (2) these that may finance their development internally. Seafarer tries to marry that target sustainable reasonable development “with some present earnings, which is a key software to understanding high quality and valuation of development.” We now have profiled SIGIX however would additionally commend the youthful Seafarer Abroad Worth in your consideration. |